Warren Buffett’s annual letter to shareholders as the CEO of Berkshire Hathaway is required reading for those in the investing world. As the greatest investor of all time, you would be wise to pay attention when he has something to say. That said, though, what if I told you Buffett’s Berkshire Hathaway letters are not the best investor letters out there? Blasphemy! Crazy! Mike has lost it! Well, I may be nuts but there is a better set of investor letters out there:

Warren Buffett’s annual letter to shareholders as the CEO of Berkshire Hathaway is required reading for those in the investing world. As the greatest investor of all time, you would be wise to pay attention when he has something to say. That said, though, what if I told you Buffett’s Berkshire Hathaway letters are not the best investor letters out there? Blasphemy! Crazy! Mike has lost it! Well, I may be nuts but there is a better set of investor letters out there:

Warren Buffett’s partnership letters.

Now you are thinking I’ve confirmed my crazy status by first saying that Buffett’s letters are not the best followed by proclaiming Buffett’s letters are the best. Well, you’d be right if it wasn’t for one subtle difference – I’m talking about the Buffett Partnership letters to investors, not Berkshire Hathaway’s letters. The Buffett Partnership is the first investment fund started by Buffett after his mentor, Ben Graham, retired and folded up his fund.

This is like Warren Buffett’s origin story. If you want to learn more about how someone got to where there are in life, go back to the beginning and figure out how they got there. In the case of Buffett, we have vital insight into that from his partnership letters.

Now follow me as we go back in time to the late 1950s where we visit a young, up-and-coming investor …

What Are the Buffett Partnership Letters?

In 1956, Buffett had moved back to his hometown of Omaha and didn’t have a job or even a plan to start a partnership. That changed when some of his relatives asked for his advice on what stocks they should own. He didn’t want to just sell advice, so he decided to form an investment partnership in the same way as his mentor Ben Graham. Six of Buffett’s friends and relatives put money into the fund while Buffett himself became the 7th partner after kicking in $100, bringing the grand total seed capital for the partnership to $105,100. At the age of 25, Buffett became the portfolio manager of his first fund.

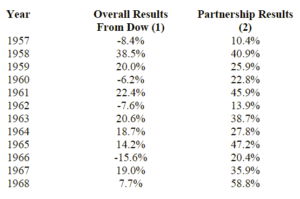

In 1969, Buffett decided to close down the partnership after years of crushing the market because he believed the returns he achieved over those years were no longer attainable. But during those years, as he does every year with his annual Berkshire Hathaway letter, Buffett regularly communicated with his investors about the portfolio and what he was seeing in the market. The result is we have a record of how the buy side GOAT thought about investing in his formative years. And it is during this time that he beat the market into oblivion. Here are the annual returns of the partnership compared to the Dow clipped straight from the source:

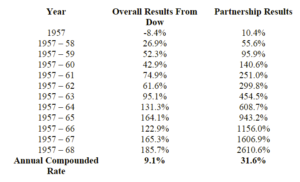

And here they are cumulative with compounding:

Despite being difficult to read, the numbers above are so absurd they are almost comical. Yet, his stated goal was to beat the Dow by 1,000 basis points annually. If you said that was your goal to a potential client today, they’d laugh you out of the room.

In the letters, Buffett often writes about the “Joys of Compounding” interest, which means to invest your money consistently at a decent rate of return and watch your money grow over time. The returns above are a glaring example of the long-term effects of compounding as the Dow’s cumulative return over the time period was “only” 185.7%, which is a respectable 9.1% per year. However, Buffet’s gaudy 31.6% per year accumulated to a 2,610.6% returns, which is 14 times what the Dow returned!

“Show me a good loser, and I’ll show you a loser.”

To start off, why haven’t other investors been able to match the record of Buffett or his Superinvestors of Graham and Dodd-ville? Buffett gave his take on the subject in the letters with three primary reasons:

-

Group Think – Buffett saw too many managers conforming to the policies and actions of their peers in the business. If everyone looks the same, everyone will get the same results.

-

Playing it “Safe” – Being contrarian is seen as a “risk” to most managers, however, Buffett saw it as an opportunity provided you’ve bought at an attractive price and have done your homework.

-

“Irrational Diversification” – Buffett didn’t diversify, or “hug the benchmark” in today’s parlance because there aren’t enough ideas out there with high probabilities of outperforming. Big winners are rare … so you’d better take a concentrated position in that name.

Buffett’s take on investing is summed up in the old adage that it is “simple, but not easy.” All Buffett did was acquire large positions in undervalued companies with evidence that will be corrected at some point. Sounds easy, but it’s not. The letters are long but well worth the read. If you need the TL;DR version, though, here are a couple of key takeaways I would highlight.

Play the Long Game

This is a theme that comes across many times throughout the letters. Buffett is a very patient person when it comes to investing. In fact, he even wrote that he considered the “buy” part of the equation to be 90% of the game. As long as he bought at the right price, he knew the stock would pay off someday. It’s also why he always said, “Price is what you pay, value is what you get.”

He also emphasized the long game with a golf analogy: “There will be some good holes and some bad holes, but the important thing is to break par for the entire round.” The same is true when investing in stocks as you will never get every stock pick right but rather, like a casino, you want to tilt the odds in your favor through better analysis.

Finally, recall the “Joys of Compounding” earlier, Buffett was looking far into the future even in his 20s. You’d be wise to do the same …

Volatility – “If it gets silly enough in either direction, you take advantage of it.”

Buffett has always seen stock prices as an asset to be utilized if desired, as ascribed to the Mr. Market analogy first given by Ben Graham. This quote from The Intelligent Investor sums everything you need to know about day-to-day market volatility:

“The true investor can take advantage of the daily market price or leave it alone, as dictated by his own judgment and inclination. He must take cognizance of important price movements, for otherwise his judgments will have nothing to work on. Basically, price fluctuations have only one significant meaning for the true investor. They provide him with an opportunity to buy wisely when prices fall sharply and sell wisely when they advance a great deal. At other times he will do better if he forgets about the stock market and pays attention to the operating results of his companies.”

If a tree falls in the woods, does it make a sound? Yes, it does, but you didn’t hear it. The same thing occurs with stock volatility – what if you opened the Wall Street Journal only once a year, would there be any volatility?

Be Different

As noted above, Buffett believed the typical portfolio manager got things wrong by copying their peers and being unwilling to stand out. To this day these stocks are known as the “crowded trades” that everyone seems to own. Back then portfolio managers usually bought only blue chip names while Buffett liked to say he invested “less conventionally.” Basically, being conventional yields conventional results.

Is this a risky strategy? I leave you with this quote to understand what Buffett would say to that question: “You will be right, over the course of many transactions, if your hypotheses are correct, your facts are correct, and your reasoning is correct. True conservatism is only possible through knowledge and reason.”